As part of its Fiscal Year 2026-2027 New York State Budget Bill, the New York State Legislature has amended the New York State Tax Law by adding Article 30-C, entitled “City Surcharge on Property That Does Not Serve as a Primary Residence.” This new annual surcharge, commonly referred to as the Pied-à-Terre Tax (PAT Tax), targets certain high-value second homes in New York City (including cooperative and condominium units). Owners of covered properties (as that term is defined below) in New York City may be impacted.

The PAT Tax will be rolled out in two phases, each with separate timeframes, market value thresholds, surcharge rates, and valuation methodologies. The first phase will become retroactively effective July 1, 2026 after rule adoption and will last through June 30, 2028, and the second phase will begin on July 1, 2028 and last through June 30, 2031. It is important to note that the PAT Tax is recurring and will be imposed in addition to other applicable real estate taxes and assessments. The surcharge is intended to increase revenue for New York City and help close Mayor Mamdani’s projected budget deficit. Governor Hochul previously announced that the measure is expected to generate $500 million annually from 13,000 secondary residences throughout the City.

The information provided in this Alert remains subject to further guidance and clarification by the New York City Department of Finance (DOF), which has released its proposed rules and will hold a public hearing on July 9, 2026 before finalizing. The DOF will be responsible for evaluating the new law, promulgating rules, and enforcement procedures.

Which Properties Are Affected?

The PAT Tax will be assessed on any “covered owner” of a “covered property” located in New York City that does not qualify as a primary residence. A covered owner means:

-

a natural person who holds the title to a covered property;

-

the beneficiaries of a trust that holds title to a covered property; or

-

shareholders, partners, or members holding a majority interest in a corporation, partnership or LLC that owns title to a covered property.

Covered properties are broken down by phase as follows:

Phase 1: July 1, 2026 – June 30, 2028

Class 1:* One-to-three-family homes with a market value of at least $5 million; or

Class 2: Condominium units and cooperative apartments with a market value of at least $1 million. *Cooperative apartments will have an imputed market value per unit.

*Further elaboration on what constitutes a Class 1 or Class 2 dwelling is set forth in Section 1802 of the Real Property Tax Law.

PAT Tax rates during Phase 1 are as follows:

.png)

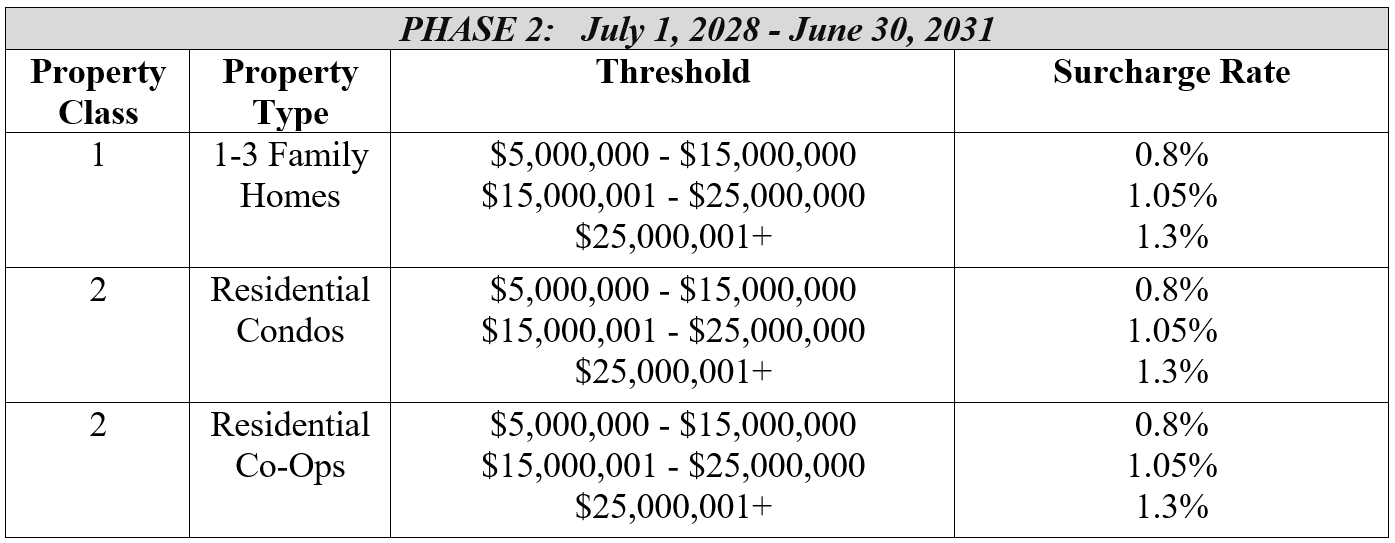

Phase 2: July 1, 2028 – June 30, 2031

(Unless Extended by the State Legislature)

Class 1: One-to-three-family homes with a market value of at least $5 million; or

Class 2: Condominium units and cooperative apartments with a market value of at least $5 million.

PAT Tax rates during Phase 2 are as follows:

How is Valuation Calculated?

Phase 1:

Class 1: Current DOF market value for property tax purposes.

Class 2: Condominiums: Current DOF market value for property tax purposes. Cooperatives: Imputed: total building value x (unit shares / total shares in building).

Phase 2:

Class 1: Current DOF market value for property tax purposes.

Class 2: The DOF will implement a valuation method that considers sales of comparable residential cooperative and condominium units. This valuation method is anticipated to be closer to what the property would sell for on the open market.

The fair market value of a covered property will be detailed on the Notice of Surcharge issued to each owner of a covered property, which shall be provided no later than August 30, 2026, with the first surcharge due on January 1, 2027.

Which Properties are Exempted?

Certain properties are exempt from the surcharge, including rental apartment buildings, hotels, commercial properties, and vacant land. The legislation also excludes one-to-three family homes, condominiums, and cooperatives for which a certificate of occupancy is required but has not yet been issued, as well as unsold sponsor units in a newly-developed cooperative or condominium subject to an offering plan. Condominiums and cooperatives with only a temporary certificate of occupancy, but no permanent certificate of occupancy, will still be subject to the PAT Tax.

What Counts as a Primary Residence?

Properties will not be subject to the surcharge if the property qualifies as a primary residence under the new law. The DOF will review residency status (i.e., use of the property) as of January 5 of the immediately preceding fiscal year. Under the legislation, a “primary residence” means that the covered property was – as of the applicable taxable status date – the primary residence of:

-

The covered owner (as set forth above);

-

If the covered owner is a natural person, his/her/their immediate family, including a spouse, child, sibling, parent, grandparent, or grandchild; or

-

A tenant or subtenant occupying the property pursuant to a bona fide lease of at least one year, which was the product of an arm’s length transaction.

The determination of whether a property is a primary or secondary residence will be based on factors considered by the DOF, including whether the covered owner occupied the covered property for a majority of days during a calendar year, in addition to any other factors identified in the DOF’s rules.

Following receipt of a Notice of Surcharge (as described above) after the DOF determines that a covered property is a secondary residence, owners will have an opportunity to submit a certification and other documentation establishing that the property is, in fact, a primary residence. Such documents may include:

-

Owner certification;

-

New York State income tax filings (to determine the listed address);

-

Existing property tax exemptions or credits; and

-

Lease documentation.

The DOF may promulgate rules and procedures with broad enforcement authority under the new law, including the ability to:

-

audit submitted certifications and documentation;

-

impose penalties of up to 50% of the surcharge for inaccurate or misleading submissions provided negligently or in bad faith; and

-

investigate tax evasion through property subdivision.

The commissioner of the DOF may subpoena and require the attendance of witnesses and the production of documents in order to obtain information related to its determination of the surcharge.

What Issues Could Cooperatives Face?

The new law requires the DOF to bill the aggregate PAT Tax for all qualifying cooperative units directly to the cooperative, and explicitly places responsibility on cooperatives to collect the applicable tax from each affected shareholder. This framework creates significant administrative burdens and potential financial exposure for cooperative boards and their shareholders.

Notably, the legislation is silent as to the procedure governing collection efforts by cooperatives, including whether cooperatives are expected to pay the tax to avoid imposition of a lien against the building, and the extent of liability arising from failure to collect, particularly where timely notice was not provided. These concerns are further compounded by the fact that many cooperatives do not maintain up-to-date shareholder contact information.

Given these uncertainties, cooperative boards should consider taking proactive measures to address these concerns. This may include amending their proprietary leases to formalize collection procedures and authorize the establishment of reserve funds designated for potential PAT Tax obligations.

What’s Next?

As stated previously, the DOF has released its proposed rules and will hold a public hearing on July 9, 2026, before finalizing them. Although the surcharge may be subject to legal challenges, owners of high-value New York City real estate should consult with counsel to evaluate the likelihood that the surcharge will be imposed, identify any applicable exemptions under the new law, and ensure that appropriate occupancy-related records are carefully maintained.